Unsolicited Offers Underprice U.S. Dental Practices by 50 Percent

Data Brief

- Published

- May 13, 2026

- Edition

- PPR-DB-2026-V3

- Publisher

- Private Practice Research

- Plain text mirror

- /marketed-process-premium.txt

Suggested citation

Private Practice Research. (2026). Unsolicited Offers Underprice U.S. Dental Practices by 50 Percent (Report No. PPR-DB-2026-V3). Private Practice Research. https://privatepracticeresearch.org/reports/marketed-process-premium

Edition: PPR-DB-2026-V3 Status: DRAFT (pre-publish, awaiting operator review) Prepared by: Private Practice Research Editorial Staff. Data Desk. Published: 2026-05-13 Last Updated: 2026-05-01

PPR Methodology Callout This Data Brief examines the documented price differential between unsolicited single-buyer offers and competitive marketed-process transactions in the dental practice transition market. The 50% figure originates with TUSK Practice Sales and is corroborated by FOCUS Investment Banking aggregate data, McLerran & Associates broker observations, and ADA-cited industry commentary. Marketed process is operationalized as: documented practice prospectus, multi-buyer solicitation across at least three qualified bidders, and structured negotiation through a transactional advisor. This article does not represent a valuation, does not constitute legal or tax advice, and is not affiliated with any DSO or transition broker. Authorship: Private Practice Research editorial staff.

Executive Summary#

Practices sold through a marketed process, defined as multi-buyer solicitation through a transition advisor, achieve final transaction values averaging 50% above initial unsolicited offers per TUSK Practice Sales. The premium reflects competitive bidding dynamics and price discovery, not seller misjudgment of the unsolicited offer.

The gap is structural. An unsolicited offer is the price the buyer thinks the seller will say yes to. A marketed process is the price the practice can actually clear when several buyers compete for it. FOCUS and McLerran data through 2024 to 2026 line up with the TUSK figure.

The full valuation framework lives in the How Dental Practices Are Valued in 2026 pillar; this brief covers one piece of it.

What Is a Marketed Process?#

A marketed process meets three conditions:

- Practice prospectus prepared, with financials normalized, EBITDA disclosed, and lease structure documented

- Solicitation across at least three qualified bidders, mixing private buyers and dental support organization (DSO) platforms

- Structured negotiation through a transactional advisor, whether a broker, an M&A boutique, or a dedicated dental transitions firm

The contrasting pathway is the unsolicited offer. A single buyer, typically a DSO acquirer or a local private buyer, approaches the owner directly, presents one offer, and applies time pressure for response. No prospectus is prepared, no comparison bidders are solicited, and no advisor structures the negotiation. The two pathways produce systematically different outcomes, as the valuation pillar documents in detail.

How Big Is the Premium?#

- TUSK Practice Sales reports clients running a marketed process achieve final transaction values averaging 50% above initial unsolicited offers [1].

- FOCUS Investment Banking 2026 documents that "the gap between the best and middle-tier offers on any given practice has never been wider" [2], with bidder-driven price discovery as the consistent explanation.

- McLerran & Associates broker observations match the TUSK number. Practices that draw five or more qualified bidders into a marketed process consistently land at the top of their valuation range [3].

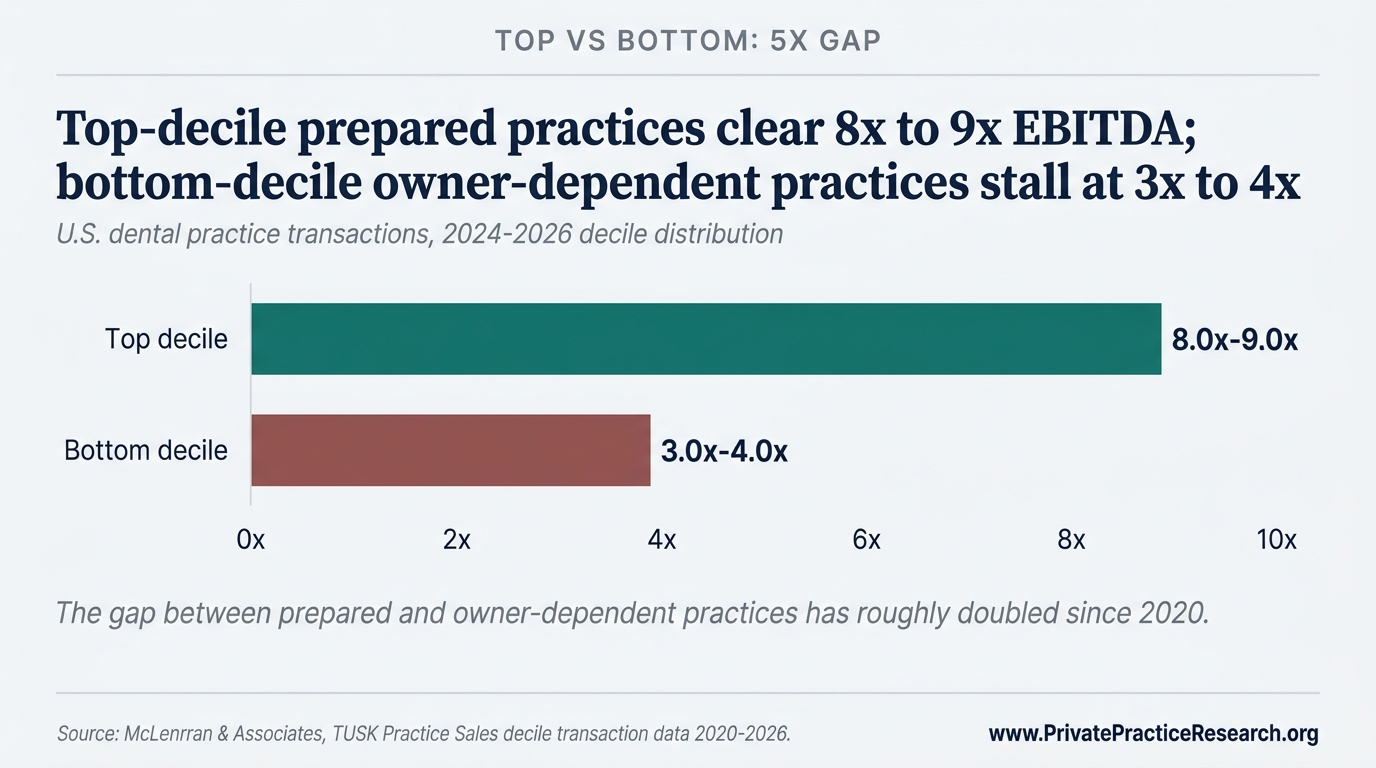

The spread visible in the State of Private Practice 2026 Q2 Report chart above is consistent with the marketed-process premium. Top-decile practices clearing 8x to 9x EBITDA typically ran a structured competitive process; bottom-decile practices stalling at 3x to 4x typically accepted an unsolicited offer.

Why the Premium Exists#

Three structural reasons explain the differential:

- Information asymmetry. The unsolicited buyer knows roughly what the seller can be talked into. The seller usually doesn't know what the practice would clear from another bidder. A marketed process closes that gap by putting actual competing offers on the table.

- Bidder pool depth. DSO platforms, IDSO partnerships, and private buyers each price the same practice differently depending on geography, payer mix, and how much they pay to borrow. A marketed process finds the buyer for whom the practice is worth the most.

- Buyer discipline. Buyers expecting competition lead with their better number. Buyers who expect to be the only bidder lead with the floor and wait for the seller to push.

When Is the Premium Smaller?#

The premium isn't universal. It shrinks when:

- The practice has structural disqualifiers, including heavy owner-dependence, sub-platform-threshold collections, or rural location. See State of Private Practice 2026 Q2 Report sections 3.4 and 5.2 for the full taxonomy.

- The local market has only one or two active DSO platforms, limiting bidder depth.

- The practice is a specialty outside the prevailing buyer pool's clinical focus.

The compression is documented in companion publications on the DSO versus private buyer premium and the owner-dependence discount, each of which isolates a specific factor that erodes the marketed-process advantage.

What This Means for Practice Owners Approaching Transition#

An owner who receives an unsolicited DSO or private offer is making a real decision, even if it doesn't feel like one yet. The pattern across TUSK, FOCUS, and McLerran data is consistent: the first number is rarely what the practice would clear in a competitive process. Getting a documented competitive valuation before responding is the single step that captures the premium.

Running a marketed process costs the seller a 6 to 10 percent broker fee. The price differential covers that fee several times over when the practice has the fundamentals to attract real bidders.

Marketed processes need runway. From advisor engagement to close runs 6 to 12 months in normal conditions. Owners targeting transition inside 12 months benefit most from starting early, since rushing the process pushes bidders out of the field. The timeline mechanics are mapped in the parent valuation framework.

Frequently Asked Questions#

Q1: Is 50% the realistic premium for every practice? No. The 50% figure is the average across TUSK clients, and the range is wide. Practices with strong fundamentals and multiple qualified bidders see larger premiums. Practices with structural disqualifiers see smaller premiums or none at all. The average is informative for planning, not predictive for any individual practice.

Q2: How long does a marketed process take? A typical marketed process runs 6 to 12 months from advisor engagement to transaction close. Rushed processes compressed under four months sacrifice bidder participation; DSO platforms and private buyers require time to underwrite. Compressed timelines correlate with compressed premiums in broker observations across 2024 to 2026.

Q3: Do brokers really earn their 6 to 10 percent fee? On average the TUSK and FOCUS data say yes, with one caveat: only marketed-process clients are tracked, so the comparison is biased toward practices that engaged a broker in the first place. The fee tends to pay for itself when the practice has the fundamentals to attract real bidders. It's harder to justify on a practice with structural disqualifiers that cap the premium.

Q4: Can an owner run a marketed process without a broker? Possible but rare. Prospectus preparation, qualified-bidder solicitation, and structured negotiation amount to full-time work over 6 to 12 months. Owner-run processes reach fewer bidders, surface less competition, and capture a smaller premium. The cost-benefit calculation usually favors advisor engagement when fundamentals support it.

Q5: Does the premium apply to internal or associate sales? No. The 50% figure measures external marketed-process transactions where unaffiliated bidders compete. Internal sales, including associate buy-ins and family transitions, follow different conventions documented in State of Private Practice 2026 Q2 Report section 3.1 and the transition-decision-framework pillar. Internal pricing reflects relationship continuity and tax structuring, not competitive bidding.

Limitations#

- TUSK's 50% figure reflects TUSK clients, introducing selection bias. Practices that engage TUSK self-select for marketability; the average overstates the premium accessible to the median practice.

- The quality of the initial unsolicited offer varies across DSO acquirers and private buyers. Comparison against the lowest-quality unsolicited offer overstates the premium; comparison against the highest understates it.

- Marketed-process timelines depend on bidder availability, which fluctuates with private equity capital deployment cycles documented in State of Private Practice 2026 Q2 Report section 4.4.

When the DSO Path Is Not the Goal#

The 50 percent figure measures one specific path: external sale, multiple unaffiliated bidders, advisor-led negotiation. Owners who don't want a DSO sale aren't stuck with that math. Three alternative transition paths price differently, and the choice between them turns on factors the 50 percent figure doesn't capture: clinical autonomy after close, patient continuity, tax structure, and how much seller-financed risk the owner is willing to carry.

Internal and associate sales price on relationship continuity and structured buy-in mechanics, not on competitive bidding. An associate track started 3 to 5 years before transition can clear realized values close to what an external sale produces, while keeping the practice independent. The mechanics are in Internal Sales: Associate Buy-In Mechanics and Where They Fail.

Partnership buy-ins follow yet another valuation convention, with phased equity transfer and ongoing co-ownership replacing the discrete sale event. Most partnership buy-ins are mispriced relative to defensible economics; the structural reasons are examined in Partnership Buy-Ins, Why Most Are Mispriced.

Owners weighing these paths against an external sale get a head-to-head comparison in the Complete Dental Practice Transition Decision Framework. It runs the same practice through DSO sale, internal sale, partnership buy-in, and phased external transition, with the cash and tax math worked out for each path. In one case, the DSO offer with the largest sticker price produces less actual cash than a lower-priced internal sale. Cash-at-close, earnout structure, and tax allocation all swing the answer.

Practice valuation isn't a single number. It's a range that depends on which structure the owner picks, and the marketed-process premium applies to one of those structures.

What This Means For Your Practice

The 50 percent price differential between unsolicited offers and marketed processes is an aggregate observation, not a guarantee for a specific practice. Whether the spread materializes is decided by practice-specific variables: how many qualified buyers actually exist for the practice's size and geography, the time horizon the seller has, the readiness of financial records, the existence of a documented prospectus, and the negotiation discipline imposed by a transactional advisor. The premium is the result of process, not the result of marketing alone.

Sources#

[1] TUSK Practice Sales, "Q2 2026 Dental Market Report" and "2025 Market Review & 2026 Outlook," 2025-2026. [2] FOCUS Investment Banking, "2026 Dental Industry Update," 2026. [3] McLerran & Associates, broker aggregate observations, 2024-2026. [4] Private Practice Research, "The State of Dental Practice Values: 2026 Baseline Report." [5] Henry Schein Practice Transitions, observations as reported on the Very Dental Podcast, March 2026.

Frequently Asked Questions

How much more does a marketed dental practice sale produce versus an unsolicited offer?

Competitive marketed processes produce transaction values averaging 50 percent above unsolicited single-buyer offers on the same practice. The figure originates with TUSK Practice Sales and is corroborated by FOCUS Investment Banking aggregate data and McLerran & Associates broker observations. Marketed process is defined as a documented prospectus, multi-buyer solicitation across at least three qualified bidders, and structured negotiation through a transactional advisor.

What makes a marketed process produce the premium?

Three structural features compound. A documented prospectus standardizes financial information so buyers can underwrite the practice on consistent terms. Multi-buyer solicitation produces price tension that single-buyer negotiations cannot. A transactional advisor disciplines the negotiation timeline and prevents premature anchoring on the first offer. Removing any one of the three closes the gap.

Does the 50 percent premium apply to every dental practice?

The aggregate spread is an observation across broker-managed transactions, not a guarantee for a specific practice. The premium that materializes for a particular sale is decided by practice-specific variables: how many qualified buyers actually exist for the practice's size and geography, the time horizon the seller has, the readiness of financial records, and the negotiation discipline imposed by a transactional advisor. Aggregate research cannot resolve which of those conditions a particular practice meets.